Millennials Are Much Better with Money Than Baby Boomers

Photo by Hugh Pinney/Getty

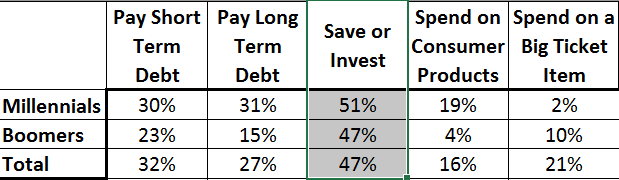

Taxes are due today, and unlike our president, we know quite a bit about what is contained in our collective returns. People across all generations spend this season fretting over how much to pay Uncle Sam and what we will do with the money we get back from the federal government. Principal Financial Group shared some of their data with Paste, and revealed that 66% of all Americans expect to receive a federal or state refund this year. A little less than half of that group (47%) plan to save or invest their refund. The divide between the generation who plunged the world into debt and the one tasked to dig out of it is reflected in their figures of what we plan to do with our refunds.

Data by Principal Financial Group

Timing no doubt factors into these numbers, as younger people have more debt and should be more focused on saving than their older counterparts, but reality doesn’t completely bear all of this basic logic out—as 79% of boomers have less than $5,000 in their savings account. In that case, they should be the ones much more focused on hoarding funds than those of us who are decades away from retirement, yet the numbers don’t reflect this as a bigger priority for boomers than it is for millennials.

{kind=link}

The largest and most immediate shift is that millennials are driving an economy away from big-ticket items—demonstrated by Principal Financial’s measly 2% figure above. Many of us graduated into a market that lost 7.3 million jobs between September 2008 and February 2010—an unthinkable level of turmoil for anyone who did not live through the Great Depression. Baby boomers grew up in a thriving economy, so they have been less able to kick the habit of buying shiny and expensive things, while we never even got a chance to sample them in the first place. Peak-home buying years used to come in our 20’s, but for millennials, that average age is 45 according to Goldman Sachs. 15% of millennials say that it is “extremely important” to own a car, while double that amount—30%—say they “do not intend to purchase one in the near future.” The Uberization of the economy is a result of decades of profligate spending, and many of us are realizing that sharing items we do not consistently use is more efficient than buying them outright and watching them gather dust.

PwC’s Employee Wellness survey revealed that while 52% of employees are “stressed out” over their finances, 64% of millennial employees feel this pressure—likely because 42% of us have a student loan and 79% with these anvils around their financial necks say they have a moderate or significant effect on their ability to meet their fiscal goals. Despite our reputation for being uncoordinated airheads, millennials display far greater discipline when it comes to budgeting than our parents. According to TD Ameritrade’s Next Generation Research report, eight in ten millennials have budgets to track their spending, compared to six in ten boomers.

Millennials are typically portrayed as arrogant do-it-yourselfers, yet when it comes to the largest purchase that most people will make in their lives, 39% of millennials say they would seek help buying a home, compared to 9% of boomers. This no-doubt reflects each generation’s level of experience with this complicated ordeal, but given that the baby boomers fell victim to the largest housing crash in modern history, the fact that over 90% still think they have it all figured out is particularly alarming.

Entitlement? That’s the buzzword most aligned with millennials, but the boomers’ entitlement mindset emerges when the topic of retirement arises. 36% of millennials say that they will retire at 65—the age when federal benefits like Medicare and social security kick in—compared to 52% of boomers. As Victoria Fillet, founder of Blueprint Financial Planning, told CNBC: “Boomers still have that union mentality, the bell rings at 65 and I’m out of here.” The data demonstrates that millennials are much more flexible when considering what is an appropriate time to retire, while boomers tend to peg it to a fixed and somewhat arbitrary number.

Millennials control around $2 trillion in liquid assets according to Wealthfront—a company that helps tech workers convert company stock into a diversified portfolio of ETFs. That number is expected to hit $7 trillion by the end of the decade. While some on Wall Street may be licking their chops at that figure, this one should keep them up at night: according to a 2015 survey by Capital One ShareBuilder, 93% of millennials stated either a lack of trust or knowledge as their primary reason for not investing their money in public markets. My father was a stockbroker for 35 years, and you can count this millennial among that 93%, as I fall firmly in the “lack of trust” column. To give you an idea of how deep my skepticism goes, I have invested some of my money in the wild west of digital currency, yet I have zero interest in putting my cash into the stock market.

The backdrop to all of this is that millennials earn less than 20% than our parents did at this stage in our lives. Granted, the fact that roughly 10% more of us have college degrees than our parents did has something to do with that—as many of them were able to start careers much earlier than we have. There are plenty of modern factors which suggest that 20% difference isn’t as extreme as it initially looks, yet none of them can explain away the obvious undercurrent at the heart of this: wages flatlined in the 1970s while productivity continued to rise.

{kind=link}

Over the last half-century, the American economy stopped working for everyone but those at the very top, and this is the only world that millennials know. Baby boomers love to rip on our generation for being selfish and bad with finances, but whether it’s data from Principal Financial Group, PwC, TD Ameritrade, Capital One, Goldman Sachs or one glance at the national debt, all signs point in a uniform direction: millennials are simply better with money than baby boomers.

Jacob Weindling is Paste’s business and media editor, as well as a staff writer for politics. Follow him on Twitter at @Jakeweindling.