Do you still not quite know what Bitcoin is or how it works? Don’t worry, neither does most of the world. But despite the confusion that continues to surround them, Bitcoin and the rest of its cryptocurrency brethren have become a growing part of internet commerce. And they don’t seem to be going away anytime soon. Depending on who you ask, that can be good or bad.

To help you form your own opinion, here are five things that everyone should know about cryptocurrency.

1. There Are a Bunch of Them

When Bitcoin launched in 2009, it was the first form of cryptocurrency. It introduced the idea of using cryptography to create a highly secure way of trading purely digital funds online. And by limiting the number of Bitcoins that can ultimately exists, it circumvents inflation in a way not unlike precious metals. However, Bitcoin’s open-source software has made its system fairly easy to replicate, and since its launch numerous competitors have arrived to challenge the Bitcoin throne. Some are even doing a pretty good job.

Meme-inspired Dogecoin is sponsoring Nascar drivers. Kanye West parody Coinye became prominent enough to warrant a lawsuit from the rapper himself. And just recently INNCoin, or IndependenceCoin, combines old school gold standards with new school cryptocurrency. There’s Peercoin, Darkcoin, Namecoin, and the list goes on. But even with all of these newcomers, Bitcoin remains the champ, at least for now. After all, it just got a football bowl named after it.

2. You Can Actually Use Them to Buy Lots of Things

Aside from Iceland and its foreign exchange freeze, cryptocurrencies are legal all over the world. However, countries like China are still a bit wary and Bitcoin trade there is subject to heavy restrictions. But besides that, plenty of places now accept Bitcoin, and not surprisingly, they tend to be businesses with strong ties to the web. Amazon, eBay, PayPal, GameStop, WordPress, Newegg, Apple’s App Store, Expedia, Subway, CVS, and OkCupid all accept Bitcoin as do traditional brick and mortar stores like Sears, Kmart, and Home Depot. Dell recently announced that they would be accepting Bitcoin, making them the largest company to accept them as currency.

And even if you choose to go down some darker corners of the internet, to places like 4Chan or The Pirate Bay, rest assured that your Bitcoins will be able to follow you there as well. Of course, you can also just blow them on some Reddit gold.

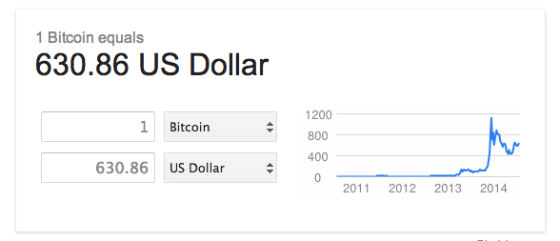

3. They are Still Kind of Unstable

Like all currency, cryptocurrencies’ value fluctuates. Even with their highly planned formulas and ultimately finite supply, they have their ups and downs. However, because of how new they are, not everyone who invested right away realized this. Bitcoin was going up so they just assumed it would go up forever and they should get in while the getting was good. It was a never-ending gold rush, until it ended.

In the past few months, Bitcoin has suffered some tremendous crashes, slashing its value in half from around $1000 per Bitcoin to $500. Some believers lost so much money that the Bitcoin subreddit felt compelled to post a link to the suicide prevention hotline to help its readers get through these tough times. However, all of these cracks in Bitcoin’s armor have just inspired legions of new cryptocurrencies to rise up and take its place. But there’s nothing to suggest that they won’t fall prey to this volatility as well.

4. No One Knows For Sure Who Made Bitcoin

Bitcoin was first proposed in a 2008 research paper by someone named Satoshi Nakamoto. However, no one has yet been able to track down and fully confirm whether or not Nakamoto is even a real person. And as Bitcoin’s fame rises, its mysterious creator has become something like an internet folk legend. Theories range from the mundane like “it’s a pseudonym for Nick Szabo or Hal Finney” to full-on conspiracy crazy like “it’s an acronym for a Japanese corporate cabal controlled Samsung, Toshiba, Nakamichi, and Motorola.”

Earlier this year, Newsweek confronted a man named Dorian Prentice Satoshi Nakamoto and thought they had finally cracked the case. However, this Nakamoto denied any connection to Bitcoin, and days later, the typically silent Nakamoto P2P Foundation that started this whole mess released a statement saying, “I am not Dorian Nakamoto.” So the hunt continues. Is there really a Satohsi Nakamoto? Maybe he’s just in our hearts. Either way, the anonymous nature of cryptocurrency remains one of its most valued properties.

5. It Won’t Be a Libertarian Playground Forever

With its lack of regulation and connection to the government, it’s no wonder that cryptocurrencies have become so beloved by libertarians, anarcho-capitalists, and people who just really want to end the Fed. However, even with its relative amount of extra freedom, jumping head first into cryptocurrencies won’t completely shield you from Uncle Sam. After shutting down Silk Road, the infamous online marketplace for illegal goods like drugs and weapons, the US government seized $25 million in Bitcoin this January that it then proceeded to auction off. And before that, they had seized and froze assets from traders like Mt. Gox, what had been the largest source of Bitcoin transactions. Many also believe that Mt. Gox’s subsequent bankruptcy led to the apparent suicide of Autumn Radtke, CEO of First Meta Bitcoin Exchange.

So what’s the lesson to learn from all this? Just because Bitcoin, Dogecoin, and cryptocurrency in general may initially seem like shiny, new internet magic, be sure to approach them with a healthy amount of skepticism and know that just because they are unregulated as of now, it may not stay like that forever.