What’s the Real State of the American Economy in 2016?

Photo courtesy of Getty

Is the economy in good shape?

Nearly every election revolves around that loaded question, as American politics projects a fraudulent image of the captain of the public sector as someone in complete control of the private sector. The central job of the President is foreign policy, as Bruce Blair, a Princeton University scholar on global security, recently explained:

[If the president] “gave the command [to launch nuclear weapons], his executing commanders would have no legal or procedural grounds to defy it no matter how inappropriate it might seem.”

Donald Trump has reminded all of us that more is at stake this year than just the usual haggling over percentage points on the GDP between Team D and Team R. The outsized importance our financially compromised political parties place on the importance of taxes relative to their influence on the economy is downright laughable, as Mark Cuban clarified on his blog in 2011:

Companies hire because they need people to compete and keep customers happy, not because of lower tax rates. The same principle applies to hiring. It is incredibly expensive to hire people. You hire people because you need them. You don’t hire them because your taxes are lower. You don’t hire them because you just repatriated cash from a foreign country. You hire them because you have a specific need for them. They are going to help you become more profitable, more productive, more competitive, whatever the reason. No one hires people simply because they have some more cash in the bank… Bottom line is that while CEOs of public companies and financial engineers have good reasons to ask for lower taxes, I don’t see lower taxes creating jobs.

Returning to the loaded question to begin this piece – let’s travel exactly 8 years back in time. Sarah Palin was rootin and tootin and hollerin and hootin all over “Real America,” and actual America began to think that the GOP might be losing its damn mind. The stirring rhetoric of one of the most centrist Democrats of my lifetime inspired a generation of progressives to convince themselves that this was their McDreamy. Meanwhile, the economy was making it look like Lindsay Lohan had her shit together by comparison. It is genuinely infuriating to see so many take for granted how close we were to the edge of oblivion. As Henry Paulson, Treasury Secretary at the time told CNBC:

“This was a massive credit bubble that burst and I just think this was a major dislocation. We’re fortunate to be where we are right now…This was a 100-year storm. These excesses had been building for years and years.”

Even getting a cursory understanding of the economy is difficult, but Ray Dalio gave one of the best explanations you will ever see in his video How the Economy Works. If you have a half hour to kill, that description of how cash and credit create a money orgy to fuel our economy is one of the simplest explanations of the most complex and interconnected entity the world has ever known.

The nature of a capitalist economy runs in cycles, more commonly known as boom and bust. The economy accelerates, confidence grows, and people borrow more money to put into other people’s pockets: my spending is your income. Debt payments inevitably come due, and begin to strip the gains down brick by brick, ultimately reaching a critical mass that results in a collapse of confidence and lending, leading to less fuel for the economic engine. The low point in this cycle is the main reason why the Federal Reserve exists, as it serves as the lender of last resort – stepping in when the private sector is too weak to carry the tremendous weight that our economy brings. The economy actually moves along two concurrent cycles – short and long. Short cycles bring recessions, and long ones bring depressions. As Hank Paulson said, this was a one-hundred-year storm. We were due, and the additional excesses and greed foisted on the economy by a generation of Gordon Gekko wannabes resulted in an explosion of titanic proportions.

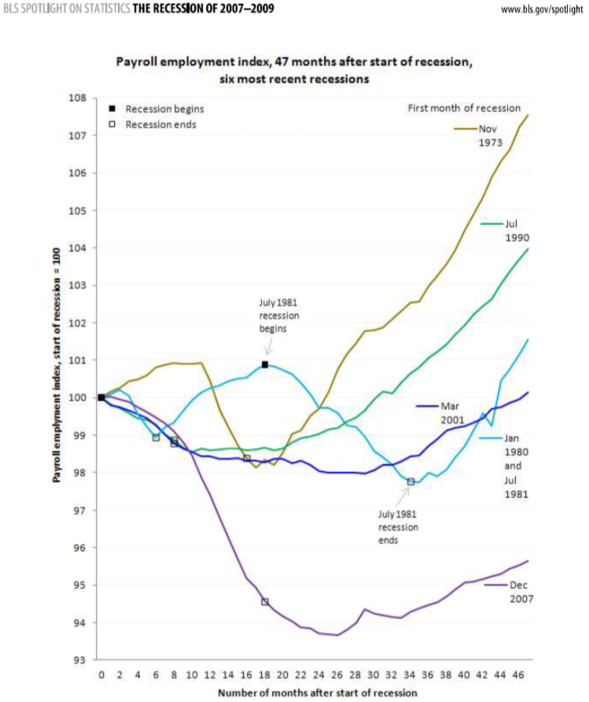

The economy shrank four quarters in a row, with two contracting more than 5%. Q4 2008 fell 8.effing2% – more than any other recession since the Great Depression. Unemployment rose above 12% in California and hit 15% in Nevada. From October 2008 to March 2009, we lost an average of 712,000 jobs per month. Between January 2008 and February 2010, employment fell by 8.8 million—the largest absolute decline since the Bureau of Labor Statistics began their CES survey of the economy in 1939. The previous record was 4.3 million net jobs lost from November 1944 to September 1945, and unlike the recessions of the last 40 years, those jobs did not come back quickly.

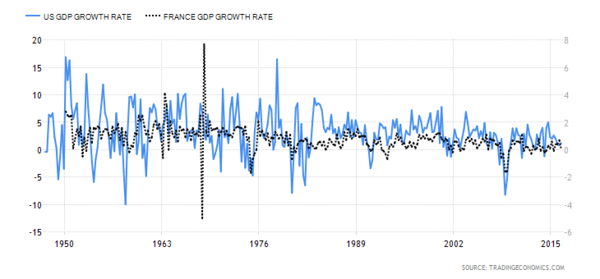

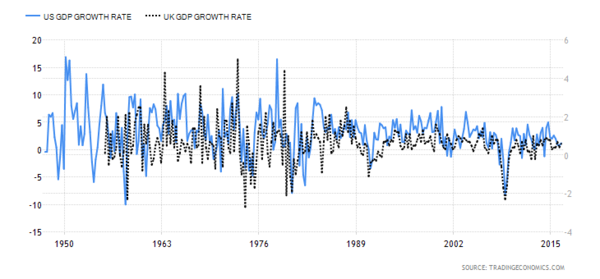

The Great Recession is the all-time leader in every horrifying statistic from the studies borne out of the Great Depression. 2008 fell on a long cycle and was dramatically exacerbated by shady lending at the heart of the American lie: buy four walls and a picket fence and your investment will never lose value. History tells us it usually takes an economy about a decade to recover from a binge like this, and we still have (at least) two years to go. We should temper our expectations. Besides, the data shows that relative to our peers, we’re in good shape. For example, France and the UK’s economies are quite literally the poor man’s version of the USA’s.

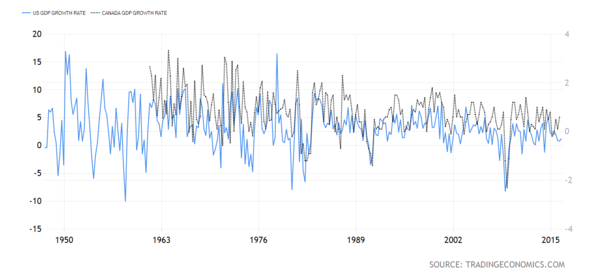

Granted, there is one peer who surpasses us. Our friends up north can comfortably call themselves the West’s grownups now. The rest of us are run by the adults from South Park.

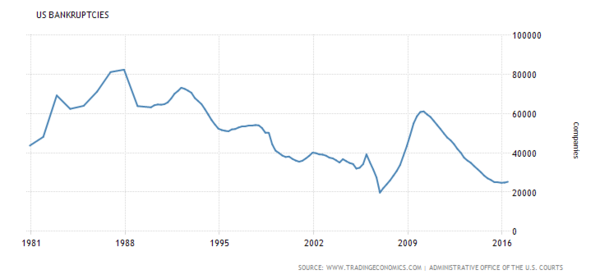

And despite Gronk spiking six years ago, bankruptcies are at a thirty-five year low.

Even though 2% annual economic growth sounds sluggish, Warren Buffett provided a back of the envelope calculation in a 2015 letter to his shareholders to explain how 2% growth is actually a good thing:

America’s population is growing about .8% per year (.5% from births minus deaths and .3% from net migration). Thus 2% of overall growth produces about 1.2% of per capita growth. That may not sound impressive. But in a single generation of, say, 25 years, that rate of growth leads to a gain of 34.4% in real GDP per capita. In turn, that 34.4% gain will produce a staggering $19,000 increase in real GDP per capita for the next generation. Were that to be distributed equally, the gain would be $76,000 annually for a family of four.

However, all this growth certainly is not going to the vast majority of the population. Bernie Sanders claims that 99% of all new money since the Great Recession went to the top 1% (according to that liberal rag the Wall Street Journal, it’s 95%). University of California Berkley professor Emmanuel Saez, who has provided a big chunk of the economic data which Sanders’ campaign was predicated upon, asserted that the figure was 91%. Regardless, we’re arguing how much dressing we want on our shit sandwich, the immediate “recovery” out of the Great Recession was only felt on balance sheets, not in wallets.

However, that overwhelming figure stopped being true in 2012, when things finally began to break for the proletariat, as 2014 and 2015 were “the first two years where bottom 99% incomes finally started to grow significantly” according to Saez, and “from 2009 to 2015, average real income per family grew by 13.0%, but the gains were uneven. Top 1% incomes grew by 37.4% while bottom 99% incomes grew only by 7.6%. Hence, the top 1% captured 52% of the income gains in the first six years of the recovery.” (Emphasis added)

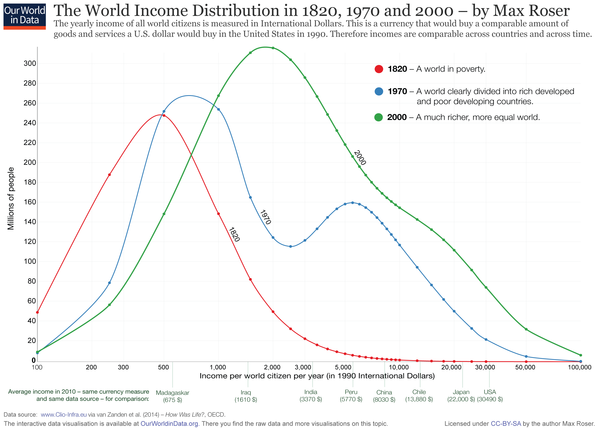

Despite remaining grossly unequal, the world is getting better. Things certainly aren’t perfect, but this hellscape depicted at the RNC of government regulators decapitating businesses and giving all their hard earned money to “those people” doesn’t exist. Bernie Sanders is 100,000% right on inequality, but his overall view of the economy is much more negative than the data suggests. Globalization has dramatically restructured the nature of the global economy, as America lost its perch as the manufacturing hub of the world due to our desire to pay people something resembling a living wage, but we are beginning to find ways to cope with that reality. The economy is steadily growing, and the yields on the far right of the chart below are split roughly 50-50 between the 1% and the 99%. That’s progress.

To be making gains in the struggle of our era while stumbling through the haze of a gigantic cyclical and structural debtsplosion is a tremendously good sign at a time where we need as many of those as we can get. The most popular billionaire in America, Mark Cuban, sounds closer to Marx than Trump, as he wrote to S.E. Cupp, Republican journalist and self-professed political Cuban fangirl:

“Just because the employer chooses not to accept the cost or risk doesn’t mean the risk and cost no longer exist. They have just pushed the risk on to everyone else. Of course, the argument could be made that the employee created the risk in the first place and should accept responsibility. But we all know that not all are able to accept that which they create. (This) creates the moral and financial dilemma for us all. How do we hold people responsible for their actions without shooting ourselves in the foot by shifting the risk from corporations to all Americans who will suffer from undereducated, undernourished, overweight children who are more likely to have any number of other problems which inflict costs (financial and other) on society? The risk never leaves the system unless you pre-empt the risk when it occurs.”

Shark Tank is the most-watched TV show by families together. Entrepreneurship – the heart, brain, and blood of capitalism is alive and well. The central problem in all this is that about 50% of us vote every four years and roughly 35% vote every two years. We have abandoned our democracy to a degree where we have essentially invited the financial elite to take over. Our government is designed to be of, for, and by the people, and when only half the people can bring themselves to do the bare minimum to serve the “by” portion of Lincoln’s famous phrase, this shit will inevitably happen*

*Disclaimer: Jacob Weindling and Paste Magazine are not responsible for any destruction of any of your property as a result of reading the following excerpt from Matt Taibbi’s reporting in Rolling Stone titled “Secrets and Lies of the Bailout.”

In October 2010, Obama signed a new bailout bill creating a program called the Small Business Lending Fund, in which firms with fewer than $10 billion in assets could apply to share in a pool of $4 billion in public money. As it turned out, however, about a third of the 332 companies that took part in the program used at least some of the money to repay their original TARP loans. Small banks that still owed TARP money essentially took out cheaper loans from the government to repay their more expensive TARP loans – a move that conveniently exempted them from the limits on executive bonuses mandated by the bailout. All told, studies show, $2.2 billion of the $4 billion ended up being spent not on small-business loans, but on TARP repayment. “It’s a bit of a shell game,” admitted John Schmidt, chief operating officer of Iowa-based Heartland Financial, which took $81.7 million from the SBLF and used every penny of it to repay TARP.

Using small-business funds to pay down their own debts, parking huge amounts of cash at the Fed in the midst of a stalled economy – it’s all just evidence of what most Americans know instinctively: that the bailouts didn’t result in much new business lending. If anything, the bailouts actually hindered lending, as banks became more like house pets that grow fat and lazy on two guaranteed meals a day than wild animals that have to go out into the jungle and hunt for opportunities in order to eat. The Fed’s own analysis bears this out: In the first three months of the bailout, as taxpayer billions poured in, TARP recipients slowed down lending at a rate more than double that of banks that didn’t receive TARP funds. The biggest drop in lending – 3.1 percent – came from the biggest bailout recipient, Citigroup. A year later, the inspector general for the bailout found that lending among the nine biggest TARP recipients “did not, in fact, increase.” The bailout didn’t flood the banking system with billions in loans for small businesses, as promised. It just flooded the banking system with billions for the banks.

First off, thank you for taking the time to buy a new computer or phone just to read the rest of this column, I really appreciate it. Secondly: $%@*#@!&^!!!!!!

We wrote a $700 billion blank check in the middle of a hurricane to a handful of Wall Street executives so they could presumably buy endangered animals to beat puppies, kittens, and babies to death with so the devil would bestow an extra 4% return on their Q2 2017 dividend, and the economy still grew at a sustainable rate. That’s incredible! This sick story that definitely didn’t lead to bruises appearing all over my knuckles really does have somewhat of a happy ending (in this dystopian nightmare that we call 2016 which sometimes makes the world of Mr. Robot look like a happy place, I’m calling this a win for mankind, we need it).

There is still plenty of work to do. Our first move should be to rebuild the equivalent of the Hoover Dam for Wall Street torn down by Bill Clinton. Glass-Steagall was established in the wake of the Great Depression because the fact that FDIC insured banks and investment banks could be one and the same was one of the central causes of that calamity. Clinton’s (surely) personally financially lucrative decision busted a hole in our ceiling, causing a massive gas leak which inevitably found its way to the lit matchboxes known as sub-prime loans left out by his douchebag friends.

Based on the structural issues in the economy, we are in pretty good shape even if it doesn’t feel like it. Is the economy bad? Compared to the 1990’s – fucking duh, it’s craptacular. Compared to 2008? We’re living in a different universe, despite the fact that the deleveraging from the Great Recession is theoretically a greater burden than the deleveraging from Great Depression. Back then, cars and radios fueled the debt bubble, while this century’s version was built upon 30 year mortgages.

The reason this economy feels bad is because relative to its normal state, it is bad. But relative to where it should be less than a decade removed from a once in a lifetime event? To quote a great bald man with a natural talent for playing Bernie Sanders: pretty, pretty, prettttaaaayyy good.