Craft Beer Growth Slows Substantially in 2016, According to Year-End Numbers

The Brewers Association, the craft beer industry’s advocacy/trade group, released its year-end 2016 statistics Tuesday afternoon, confirming what the mid-year stats had previously shown us: The era of steady, double-digit craft beer growth may be over. No longer the “young, upstart” industry putting up gaudy growth numbers, craft beer has now seemingly grown large enough that those numbers are no longer feasible.

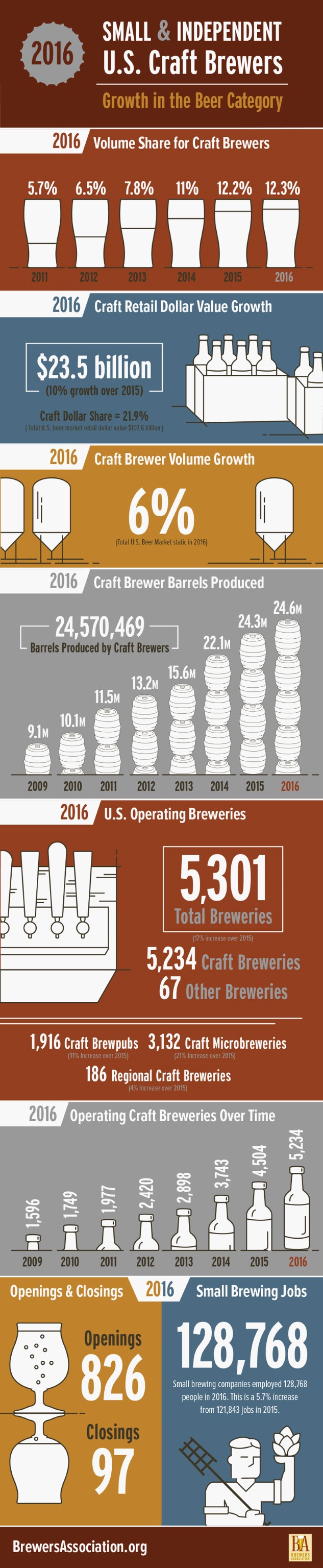

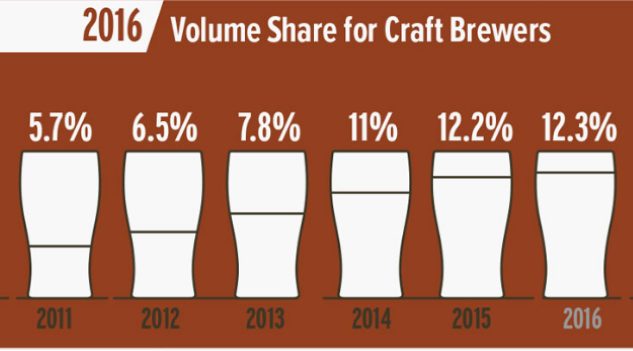

According to the BA, craft beer as a whole grew 6% in volume and 10% in retail dollar value in 2016, down from the roughly 12-15% growth it had regularly shown in recent years. That was good for a 12.3% total market share for craft beer, up only .1% from last year’s 12.2% share. Retail dollar value was estimated at $23.5 billion, representing 21.9% market share, thanks to the higher prices in the craft beer market.

However, these numbers are more complicated than they initially appear. The market didn’t simply slow down; it had some of its largest pieces removed from the board. Large regional breweries such as Lagunitas, Ballast Point and Founders are no longer included among the “craft” numbers by the Brewers Association, thanks to buyouts/changes of ownership that disqualify them, which significantly alters the numbers. Lagunitas alone would have been the #5 craft brewery in the U.S. in terms of volume, if not for the change in their classification.

As such, 1.2 million barrels of craft beer produced in 2015 was removed from play in the 2016 field, which managed to still grow slightly by adding 1.4 million barrels of its own. The total amount of craft beer produced rose from 24.3 million barrels to 24.6 million as a result. Unsurprisingly, it was the small microbreweries and brewpubs that were driving the 1.4 million new barrels of beer, account for 90% of the craft brewer growth. Closings were up slightly, to 97 breweries, dwarfed by the openings of 826 new breweries.

The picture painted by the statistics is something of a dichotomy. The smaller segment of younger, smaller breweries and brewpubs continue to grow fastest as they take advantages of market openings such as under-served neighborhoods or cities. Large regional breweries (such as New Belgium or Boston Beer Co.), on the other hand, are facing greater challenges competing with the now more than 5,300 breweries in the country, which may be cannibalizing the sales numbers of older flagship brands such as Fat Tire or Boston Lager. Bart Watson, the chief economist of the Brewers Association, commented on this in a conference call with media after the numbers were announced:

“This year was a challenging year for regional craft brewing companies; they’re facing challenges from multiple places,” he said. “They’re facing a more competitive space, with 5,000-plus breweries in the country. I’d be expecting many of those regional craft breweries to be reformulating their strategies. Regional craft breweries did grow overall, but very slowly. Moving from a regional to a super regional is much more challenging. It’s much more of a long shot than it was 10 to 20 years ago.”

This clearly speaks to a craft beer industry that has entered a period of maturation rather than its infancy. It also speaks to how strongly the acquisition of craft breweries by “Big Beer” and global breweries ends up affecting the final numbers. At the same time, it’s perfectly fair to question how much those numbers matter now—just because the Brewers Association no longer considers the likes of Founders or Ballast Point craft, does that mean they’re no longer relevant to this discussion? Does ALL ownership matter, or does it only matter when hated companies such as AB InBev and MillerCoors are involved? Some of these are questions that drinkers have to decide for themselves. Closing thoughts from Watson:

“Small and independent brewers are operating in a new brewing reality still filled with opportunity, but within a much more competitive landscape. As the overall beer market remains static and the large global brewers lose volume, their strategy has been to focus on acquiring craft brewers. This has been a catalyst for slower growth for small and independent brewers and endangered consumer access to certain brands. Small and independent brewers were able to fill in the barrels lost to acquisitions and show steady growth but at a rate more reflective of today’s industry dynamics. The average brewer is getting smaller and growth is more diffuse within the craft category, with producers at the tail helping to drive growth for the overall segment.”

Below, you can see the full statistics infographic released by the Brewers Association.