Brewers Association Data Reveals Slowing Craft Beer Growth in Depressed 2018 Beer Market

Final analysis of 2018 sales data was released today by the Colorado-based Brewers Association, confirming the trends we’ve seen in beer sales for the last few years: The craft segment is still growing, but that growth continues to slow. Meanwhile, the overall beer market continues to contract, as people drink less and less beer (and more wine and spirits) than they did the year before.

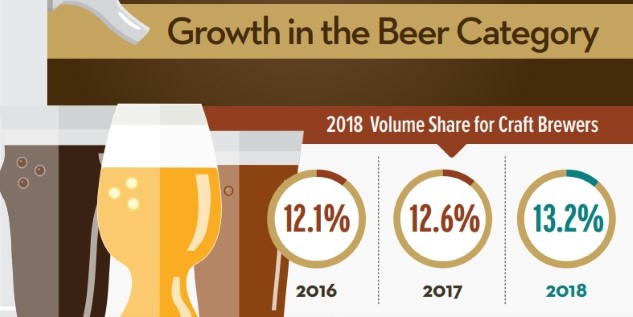

The craft beer segment, as (sometimes controversially) defined by the Brewers Association, grew 4 percent in volume in 2018, increasing the overall market share of BA-defined craft in the market to 13.2 percent. That’s up from 12.6 percent in 2017, as you can see in the snippet of infographic below. The full infographic can be viewed here. It’s certainly better than a decline, although it’s a far cry from the BA’s original goal of “20 percent by 2020,” which has long since been revised.

At the same time, retail dollar value of craft beer sold reached a new high at $27.6 billion, which represents an impressive 24.1 percent share of the dollars spent on beer—a 7 percent increase from 2017. This suggests the premiumization of craft beer pretty clearly, as consumers have purchased less beer overall, but spent more on the beer they do buy. Overall, the total beer market was down 1 percent by volume in 2018, mostly driven by the consistent, bleeding losses of major brands such as Bud Light, Miller Lite and Coors Light. Here’s hoping AB InBev and MillerCoors remain focused on suing each other over corn syrup for the foreseeable future.

Of course, these numbers have to be taken with a grain of salt in some aspects. The craft beer definition was revised again this year by the Brewers Association, ostensibly to better serve the industry, but it’s more rational to assume that the changes were made to keep Boston Beer Co., the makers of Samuel Adams, in the fold. If Boston Beer Co.’s production numbers had been allowed to leave the BA tally as a result of the company now producing more than 50 percent non-beer alcohol products (such as cider and spiked seltzer), the result could have been a decrease in total craft beer production, rather than an increase. That would have significantly changed the tone of this announcement’s headlines, as a result.

Bart Watson, the chief economist for the Brewers Association, acknowledges the industry’s growth challenges in the following quote, which was included with the announcement:

“The beer landscape is facing new realities with category competition, societal shifts, and other variables in play. There are still pockets of opportunity both in terms of geography and business model, but brewers need to be vigilant about quality, differentiation, and customer service.”

That’s the truth of this scenario: Things are fairly grim, and opportunity is present in “pockets,” rather than spades.

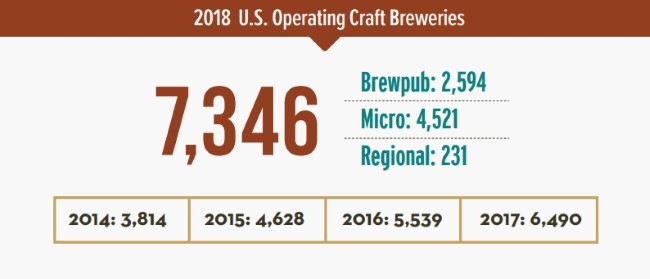

Perhaps the most concerning aspect of these numbers, though, is the fact that new brewery openings essentially didn’t slow at all in 2018. The total number of breweries increased by 856, from 6,490 in 2017 to 7,346 in 2018. That’s a 13.1 percent increase in the number of breweries operating, but only a 4 percent increase in the amount of beer sold by volume. Needless to say, it implies that there’s going to be little room for many of those breweries to substantially grow, and it only compounds the challenges faced by larger regional craft breweries, who are seeing more and more competition from smaller, more nimble brewers. If you’re a struggling Sierra Nevada or New Belgium right now, it’s hardly cheery news to see that more than 1,000 new breweries opened in 2018, with more to follow in 2019. Still, on the plus side, it does translate to an increased number of jobs in the industry—more than 150,000 in 2018, up 11 percent from 2017.

2018 also saw an increased rate of brewery closures, at 219—a number that we’ll all surely be watching closely in 2019. Will the rate of openings finally slow down, to match the slowing growth of production? Or will would-be brewmasters continue heedlessly opening new businesses in an increasingly mature market? Surely there are some opportunities still out there, of course, but this isn’t anything like getting into beer 10 years ago.

Here’s hoping for a vigorous 2019.